Small Business Insurance Cost

Small Business Insurance Cost Small Business Insurance Cost: Small business insurance refers to a collection of policies designed to protect businesses from […]

Small Business Insurance Cost Small Business Insurance Cost: Small business insurance refers to a collection of policies designed to protect businesses from […]

Health Insurance for Senior Citizens Health Insurance for Senior Citizens: As people grow older, healthcare needs naturally increase. Doctor visits become more […]

Cheapest Car Insurance for New Drivers Cheapest Car Insurance for New Drivers: Getting behind the wheel for the first time is an […]

International Travel Insurance International Travel Insurance: International travel opens doors to new cultures, business opportunities, education, and unforgettable experiences. However, traveling abroad […]

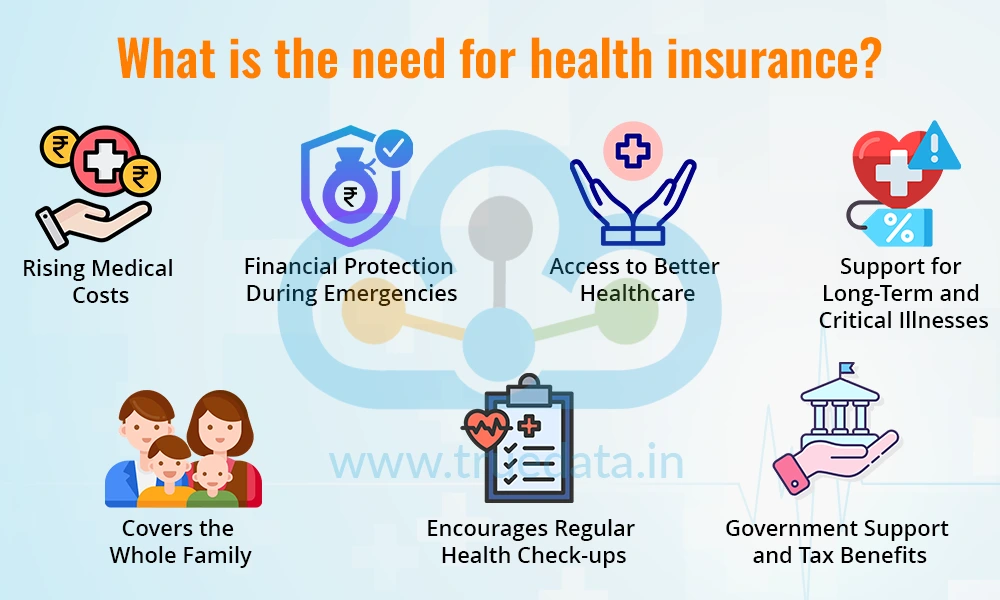

Health Insurance Benefits Health Insurance Benefits: Health insurance plays a critical role in modern healthcare systems by bridging the gap between rising […]

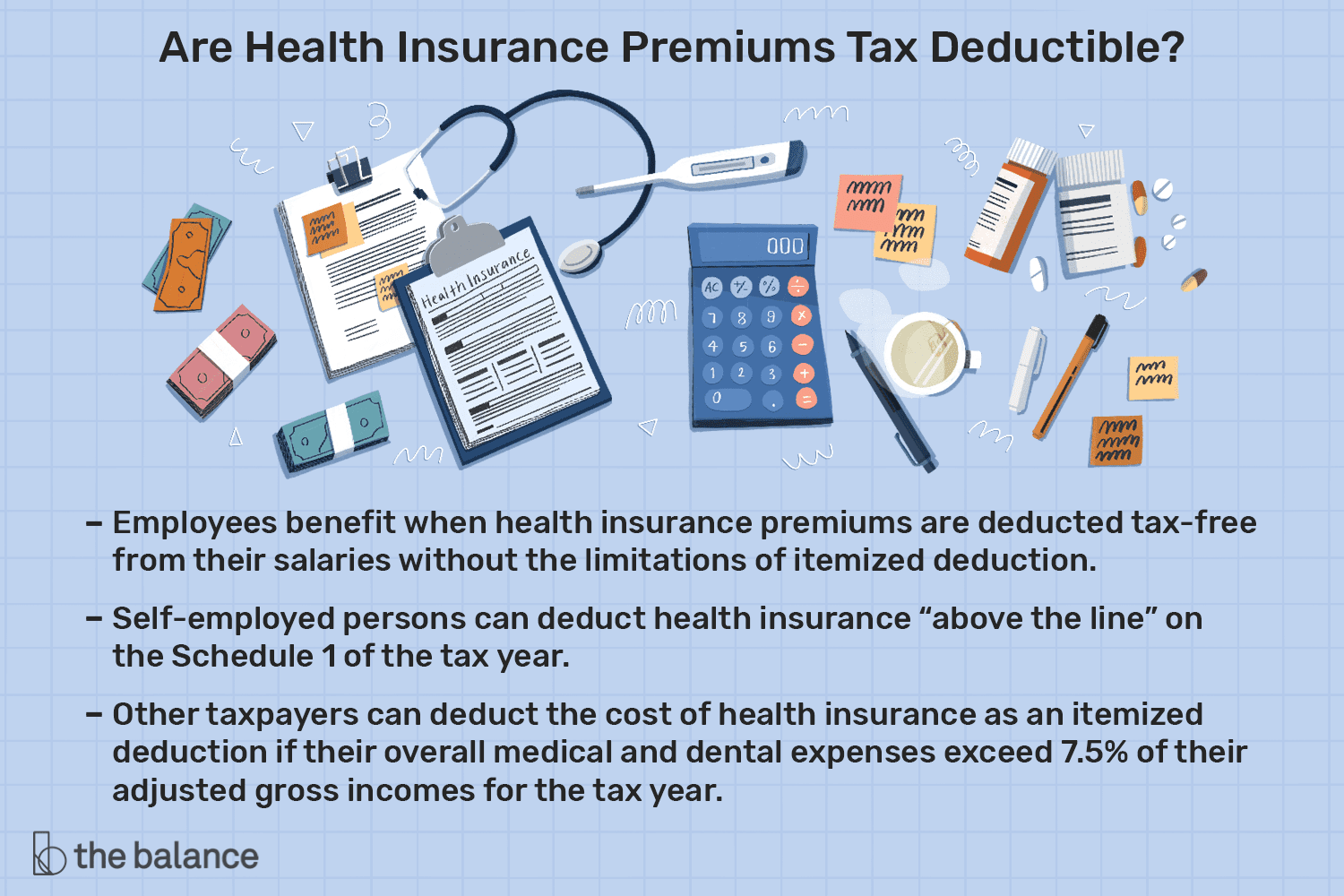

Health Insurance Tax Deduction for the Self-Employed Overview of the Self-Employed Health Insurance Tax Deduction Health Insurance Tax Deduction for the Self-Employed: The […]

Why Health Insurance Is Necessary in Our Daily Life In the United States, healthcare can change your life in a moment. […]

Health Insurance for Adult Citizens in the USA: A Detailed Guide Introduction about Health Insurance for Adult Citizens Having health insurance in […]

Usage-Based Insurance in U.S.A 2025 Updated What if the information on your auto insurance bill included more than simply your ZIP code, […]